Layer 1 Ecosystem Growth Deep-Dive

Layer 1 Ecosystem Growth Deep-Dive

A comparative analysis of the Layer 1 blockchain landscape

In the wake of the 2008 financial crisis, when all hope seemed lost, a pseudonymous cryptographer by the alias Satoshi Nakamoto sparked a revolution like no other, a digital revolution. The 3rd of January 2009 marked the creation of the bitcoin blockchain. A technology that allows for the existence of a digital native currency. A system built on the premise of transparency, censorship resistance, permissionless transactions, and trustlessness.

As the word spread, cypherpunks from across the world were fascinated by the promise of cryptographic currencies. For years people tried to iterate upon the base layer technology of a blockchain but none were successful enough to provide meaningful competition to Bitcoin.

However, just 6 and a half years later, that competition arrived. 30th of July 2015 marked the genesis of the Ethereum blockchain. Ethereum stuck to the core ethos of Bitcoin but iterated upon blockchains by creating smart contracts. Smart contracts are essentially pieces of code that that live on the blockchain which automate different processes and execute when triggered by a transaction or another contract.

These smart contracts then allowed for the creation of a whole suite of different decentralized applications (Dapps). DeFi services such as lending/borrowing, exchanges, and insurance were made possible along with NFTs, gaming, and metaverses. Ethereum was the base layer that these smart contracts exist on hence it’s given the name layer 1 (L1) chain.

Smart contracts essentially opened up a whole new set of use cases for blockchains since bitcoin simply allowed for the transfer of value through this digital currency called bitcoin.

With a whole design space now opened up, it was inevitable that Ethereum would see success, and this success eventually came. Ethereum very quickly rose to the 2nd in Marketcap. It also didn’t take long for Ethereum to surpass Bitcoin in total transaction count and the high demand for utilizing Ethereum was reflected in the high gas costs.

However, with all the success, Ethereum stumbled upon a major hurdle. The demand to use the network was way more than what the network could support.

The blockchain Trilemma

The blockchain trilemma refers to the trade-off that all layer 1 chains have to make at inception. This trade-off is between 3 factors.

· Security

· Scalability

· Decentralization

Security refers to the ability of the blockchain to operate uninterrupted. That means bugs and unforeseen errors should not halt the chain and it shouldn’t be possible to mount an attack on the network to take it down completely.

Scalability refers to the ability of a blockchain to handle transaction load. If the chain has very high demand, by how much do the gas fees increase? And how slow does the approval of transactions become? If fees increase and transaction speed decreases during high demand times, then the chain is not scalable. But if it can withstand high demand, then it is scalable.

Decentralization refers to the chain not having to depend on centralized points of control. A good indicator for this is the nodes/miners on the network. If there are more nodes/miners and they are distributed geographically, this means that the chain is sufficiently decentralized, there is no reliance on one entity which can collapse and take the entire chain down with them.

In this trilemma, all L1 chains have to choose 2 out of the 3. The hurdle that Ethereum faced was that they optimized for security and decentralization. Hence, when demand spiked from 2020 onwards, the gas fees were prohibitively expensive, and the transaction speeds were too slow.

The result was a very poor user experience.

Out of this, a new opportunity was born. There was clearly demand to use L1 chains and the different DeFi & NFT products that came along with it, but a large chunk of users were priced out. Therefore, teams from around the industry saw this as an opportunity to chip away at Ethereums market share.

The result was a whole suite of L1 blockchains spawning across the ecosystem with most of them optimizing for scalability & security while some optimized for scalability & decentralization. This kicked off the fabled ‘Battle of the L1s’ where every chain competed with one another for users, developers, and market share.

Currently, there are 40+ chains in the crypto ecosystem, with each one of them having their own set of perks and drawbacks.

The rest of this article will be a comparative deep-dive into the Layer 1 ecosystem.

EVM vs Non-EVM

For those who don’t know, EVM stands for Ethereum Virtual Machine. Put simply, the EVM is the environment under which all Ethereum accounts and smart contracts live. The sole purpose of the Ethereum protocol is to ensure that this machine, which is maintained by thousands of connected computers, is operating uninterrupted. It is the heart and soul of the Ethereum blockchain.

Given that Ethereum is the dominant L1 ecosystem, the question for all the new alternative L1s is whether they should be EVM-Compatible or not.

Being EVM-compatible simply means that the chain creates an EVM-like code execution environment. This makes It easy to interact with and move assets between Ethereum and the alternate L1, it also makes it easy for developers to port over their smart contracts from Ethereum to the new chain.

The opposite scenario is EVM incompatible chains. These are essentially chains that create their own virtual machine and execution layer that is more suited to the target audience that they are trying to cater to.

The pros of being EVM-compatible is that Ethereum has already achieved significant network effects (i.e. deep-rooted adoption) which means it’s easier for new chains to gain adoption by being EVM compatible. However, EVM is fairly constraining in terms of the types of applications that can easily be built on it. Therefore, non-EVM compatible chains typically have faster & cheaper transactions which allows them to facilitate things like GameFi or orderbook based perpetual futures exchanges.

Some examples of EVM-compatible chains include Avalanche and Fantom, while EVM-incompatible chains are L1s like Solana and Algorand. There is also this middle ground where certain L1s have an EVM compatible sidechain to simply make it easier to bring users over to their ecosystem. Examples include Aurora on NEAR and Moonbeam on Polkadot.

Under this broader technical differentiator of EVM vs Non-EVM is an entire ecosystem of L1 blockchains each of which have their more intricate set of differences.

Developer activity

A prerequisite to a well adopted L1 ecosystem is a strong developer community. Without the developers building products there would be nothing for the users to use. The developer activity is also testament to how well-built and developer friendly the chain, the native code, and the virtual machine is. The more seamless and secure it is for developers to make products, the more developer activity a chain will see.

Starting at halfway through 2015, when Ethereum was officially launched, there were only 5 L1 chains in existence with a combined developer count of 73 developers. Those chains were Ethereum, Cardano, Algorand, Binance Smart Chain, and Polkadot. Out of the 73 developers, Ethereum had 52 making them account for 71% of developer activity in the ecosystem. However, this was early days. There was not much activity on Ethereum while the other L1s were still very early in their infancy.

To get a better understanding of developer growth, we will fast forward to the start of 2020. This is when Ethereum had a well-established ecosystem of Dapps and all the alternative L1s were fully built out. This is also the time when interest in the crypto markets started ramping up with a lot of external interest from retail participants and traditional institutions alike, entering the space.

Despite so many chains being live, developer activity was still fairly concentrated amongst three chains. Ethereum, Cardano, and Polkadot had 74.5% of all developer activity at the start of 2020 with the chains having 116, 105, and 102 developers respectively. However, the following two years saw a lot of shuffling amongst developers.

From 2020 to 2021, the total developer ecosystem increased by 12% as the demand to transact on-chain began to increase. Despite the overall growth, Polkadot, Algorand, and Binance Smart Chain (BSC) saw a decline in developer activity. Outside of Ethereum, it was the trendier and newer alt-L1s at the time that saw the greatest increase in developer activity. It was Avalanche and NEAR that saw the sharpest increase with a 2300% & 61.9% increase in developer activity respectively.

However, this was still at the beginning phases of the “battle of the L1s”. At the start of 2021 is when the market entered into a peak bull mania phase. This is when overall developer activity skyrocketted. From 2021 to 2022, developer activity increased by 49.9%. Although every L1 saw an increase in activity, there were some stand out performers.

Polygon saw a 350% jump in developer activity through the year. It is technically a sidechain (i.e. a chain adjacent to Ethereum which has easy connectivity to Ethereum for security and scalability purposes) and not an L1, it does operate very similar to most alt L1s seeing that it has its own gas token and its own native ecosystem of Dapps. Throughout 2021 is when Ethereum reached the peak of its scalability issues, therefore the Polygon sidechain played a major role in allowing users to operate on a chain adjacent to Ethereum but one that is much cheaper and faster. As a result, a lot of developers flooded towards Polygon to build.

Another standout was Solana. Solana saw a 223% increase in developer activity. It rose to become the leading non-EVM chain with its proprietary consensus mechanism that allowed it to have unparalleled scalability. The cheap fees and fast transactions were unlike anything the space had seen before. This garnered the attention of more non-crypto native participants allowing them to grow a strong NFT and gaming community.

The two other standouts were NEAR and Avalanche who saw a 100% and 46% increase in developer activity respectively. NEAR & Avalanche both offered high scalability and both had EVM-compatibility, although for NEAR it was only through Aurora. This allowed many developers to easily port over their work.

2022 has been a catastrophic here for the crypto industry, but the developer stats show otherwise. The expectation would be a sharp decline in developer activity, but this activity has in fact increased albeit only by 7%.

The most popular chains of 2021 in Avalanche and Solana saw a decline in developer activity while Polygon has maintained its strength with a 37% jump in activity. The stats suggest that developer activity is now moving back to the older and more established chains presumably for security reasons, they have all been stress tested. BSC, Polkadot, Algorand, and Ethereum all saw an increase in developer activity through the year.

However, time will tell whether this increase is due to a strong belief in this industry or whether it’s a result of late hires. If the markets continue to stay weak, it is likely that these developer numbers will continue to decrease over the next year. If not, then it will be a sign of great strength for the industry.

Ecosystem growth

Directly correlated to developer activity is the ecosystem growth. Ecosystem growth refers to the number of new and unique projects that have been launched on the individual chains. The general expectation is that higher developer activity will correlate to more projects while will translate to more usage.

Seeing that Ethereum is the leading chain by marketcap as well as developer activity, lets start with it. According to DeFillama, there are approximately 566 unique projects on Ethereum, however most of them have close to no Total Value Locked (TVL) so we can trim this number down to an estimated 470 projects. After including Gaming and NFT porjects this number will increase to well over 600 projects.

The Dapps with the highest TVL in all of crypto originated from ETH and still run on ETH. Pillars of the DeFi ecosystem such as MakerDAO, Curve Finance, Lido, Uniswap, and AAVE are all Ethereum native products which have later gone multichain. These products have survived multiple stress tests and have still lasted.

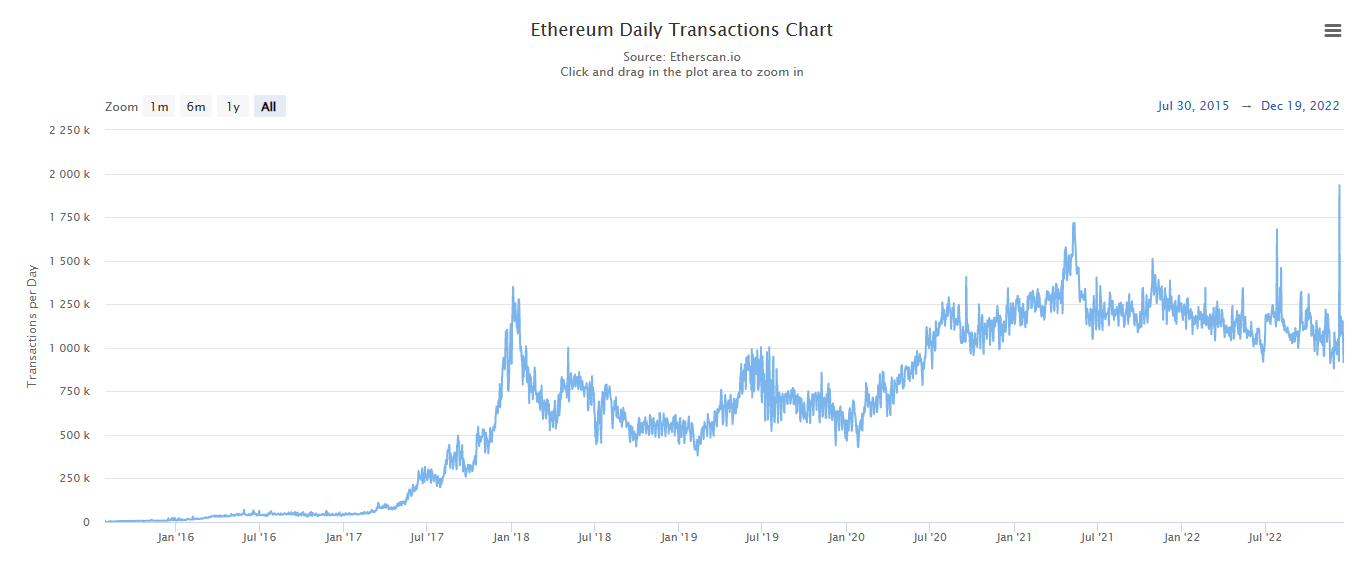

Ethereum is the most robust layer 1 chain with the highest adoption. The network has now hit 217M unique addresses with the transaction count being over 1M transactions per day since 2020.

Given the resilience and adoption of Ethereum, it can safely be said that holistically, it has the highest quality ecosystem of projects amongst all the L1s.

One of the more notable competitors to Ethereum was Solana. At its peak Solana had an estimated 607 projects running on the chain but at the time of writing this number has come down 347 as per solscan. Given the recent FTX saga and how instrumental they were in the success of Solana, a lot more projects have lost most of their treasury or been hacked, so this number in reality will be a lot lower.

However, this is mainly the DeFi ecosystem that has been affected. Luckily for Solana, they have a more Robust NFT & gaming ecosystem. According to Solscan, there have 151k new NFTs minted just this past week. Additionally, there are successful gaming projects such as Star Atlas, StepN, and Aurory amongst others which have taken advantage of the fast and cheap nature of Solana to build their games.

Currently, Solana is facing its biggest stress test yet. Fortunately, they have built a strong enough community around their NFT and gaming ecosystems to hopefully see them through. If they do make it out of these trying times then the future for Solana is bright.

Let’s move on the third competitor who also reached the top 10 at one point in time, that is Avalanche. Avalanche had a remarkable 2021 with transaction counts soaring through the year as they captured the mindshare of the crypto natives who were priced out of Ethereum. Throughout its time, Avalanche saw 133 projects get developed on the chain.

The Avalanche ecosystem mirrored the Ethereum ecosystem in almost every way and was more DeFi focused to begin with. The standout applications were Trader Joe, GMX, Pangolin exchange, and Benqi Finance. The transactions taken on these 4 applications accounted for 14% of all transactions taken place on Avalanche this year.

A marquee differentiator for Avalanche has been their scaling solution of subnets. Put simply, it essentially allows applications to operate as their own chains. This subnet architecture gave birth to a whole suite of gaming projects which became really popular for a short period of time.

Currently, liquidity has been exiting the ecosystem along with developers, but the chain has still been running as intended. Time will tell whether avalanche can withstand their stress test and make a comeback.

Polygon has been another standout performer. What started off as a sidechain has now blossomed into a flourishing ecosystem with around 400 unique projects. It has around 200M unique addresses and has facilitated a total of 2.2B transactions.

Although most of the projects are either existing Ethereum projects that have also launched on Polygon, or copies of Ethereum projects, Polygon has recently started seeing many unique and native projects come up. They have been popular amongst gaming projects and recently have seen many DEXs such as IDEX and Gains Network come up. A new wave expected to propel Polygon is decentralized social. Many Web 3 projects are looking to create decentralized social media platforms and many of them are looking to choose Polygon as their chain of choice.

Unique Use Cases

It is no secret that the crypto markets are correlated in almost every way. Even with L1s, most of the alternate L1 ecosystems could be considered copycats of Ethereum as they all had money markets, DEXs, NFT exchanges, and so on. However, the technological differences amongst the L1s mean that the technical barriers are different for each chain. This difference means that certain chains will be better equipped to cater to certain types of projects. This in itself unlocks unique use cases for some chains.

So lets go over some of these unique use cases.

Ethereums unique use case is the Layer 2 rollups. Everyone is aware of how decentralized and secure the Ethereum chain is, but without scalability, the user experience is very poor which makes a secure and decentralized chain redundant. With layer 2 rollups, and other features that are expected in the future, Ethereum can finally be scalable while maintaining their security and decentralization which effectively solves the trilemma.

Solanas unique use case is how efficient their chain is for gaming projects. Games require a high amount of transactions and Solanas architecture is among the best suited to handle such high levels of throughput. The chain has had many issues with downtime in the past. If it continues, then it is problematic, but if the problems get fixed then gaming could be a huge point of success for Solana.

Avalanche has their scaling solution which is subnets. As mentioned before, they are essentially a way for protocols to become their own chain which allows for value accrual to the token as well as much higher scalability. So far there are very few projects that have decided to go down the subnet route, but from the ones that did there have been no complaints. If they manage to get more projects onboard, subnets could prove to be a big difference maker for Avalanche.

The Unique use case for Polkadot is built in interoperability. This is achieved by having many smaller chains (called parachains) which are all linked to one another through the main chain (called the relay chain). Therefore, regardless of the purpose or use of the parachain, they can automatically be interoperable with any other parachain in the polkadot ecosystem thanks to the relay chain.

There are also unique layer 1 chains such as Arweave. The sole purpose of Arweave is storage. Arweave provides a cheaper way to store data over a much longer period of time when compared to the traditional counterparts. Arweave so far has proved to be very successful amongst, Journalists, reporters, bloggers, NFTs, and other forms of content creation/creators.

While there are many more L1 chains that exist, none of them have anything that is exceptionally different from the ones mentioned above. They all fulfil similar purposes and mainly vary in terms of degree of scalability, decentralization, and security. There is this new innovation wave in the form of modular blockchains like Celestia that are coming up, but they are not live as yet which makes it difficult to comment on them.

Biggest wins & fails of the year

With the frantic and volatile nature of these markets, it was inevitable that there would be some notable successes but also some notable failures. Unfortunately, this year was overshadowed with more failures than successes.

Starting off with the hacks and exploits. Just on Ethereum alone there was well over $1B hacked or exploited from various protocols with the ronin bridge exploit coming in at number one at $600M stolen. Solana also faced a sizable number of hacks with the Mango markets hack topping the ecosystem with $115M being exploited from the protocol. The third chain with the most hacks and exploits would be BSC facing around $300M+ worth of exploits.

Another notable failure was arguably the largest failure in the industry this year. The fall of the Terra blockchain which was an L1 that supported the algorithmic stablecoin UST whose pegged was maintained by the native token LUNA acting as the volatility absorber. The project was once at a combined $60B in marketcap, but UST went into a death spiral sending UST as well as LUNA to $0. This not only wiped out Terra but also its investors. It kicked in a contagion effect which saw almost every company in the industry go under.

Although the LUNA collapse was the biggest L1 failure of the year, there are still a few more issues of note that took place. One of them being Solana. It faced down time on multiple occasions this year where no blocks were being produced. On one occasion the downtime lasted as much as 8 hours. For a 24/7 industry that aims to onboard the masses, such levels of downtime are unacceptable. Time will tell whether these issues have been fixed or not.

Amidst the failures there has been some sign of hope. One major success has been Layer 2s built on top of the Ethereum L1. Throughout the year they have not only gained adoption with almost every project porting over to L2, but the activity has consistently been increasing through the year. Optimism launched their OP token which proved beneficial for adoption while Arbitrum maintained a steady increase in user activity without a token. With ZK-rollups starting to enter the picture with starkware and ZK-sync the outlook for the future of L2s is even brighter.

Another positive has been the user retention of some existing chains. Namely Polygon. Despite the tough market conditions, Polygon has still maintained a daily transaction count well above 2M per day through the year. This is testament to the partnerships they have made with brands such as Disney as well as the ever-growing ecosystem of DeFi and gaming applications. Expect alot more from Polygon as they gear up to launch their own EVM-compatible Zk-rollup.

Geography

Before diving into this section, it is important remember that blockchains are permissionless. This means that anybody anywhere in the world with an internet connection can use any chain of their choice. Regardless of this, the teams that build these blockchains often like to target their focus to certain markets where they think their chain will be received well.

A good way to gauge this is by seeing where conferences are held. For example, Solana and Polygon seem to target a similar sort of geography. Both of them host conferences and hackathons in Asia, with a deeper focus in India, as well as across the USA. The aim is to not only attract developers from the region, but the events act as marketing for potential users as well.

Chains like Algorand also seem to heavily target the Asian market with conferences being held in places like Singapore, Japan, India, and South Korea. However, a strategy unique to Algorand is to work with government bodies to make Algorand the chain of choice for digital assets in a specific country. This has been successful with Italy and the Marshall Islands.

Another method for checking the geographic makeup that an L1 chain has is by looking at the Telegram and discord channels. Telegram and discord are the primary ways of interacting with the community in this industry. Within discords there are separate channels with different languages but even in general chats one can see which demographic has been catered to more. For example, in the NEAR protocol chats, there were a lot more people from Asia, specifically Vietnam and Thailand.

When it comes to Ethereum, they seem to be globally recognized at this point. Their core community of contributors are from all over the world, they host conferences and hackathons all over the world, and their users are generally distributed all around the world. They were the first L1 chain in existence due to which they garnered the network effects which put them in this position. The other chains seem to be taking the approach of targeting specific important markets and then growing from there.

Suggestions

It is no secret that as the broader industry entered into a bear market that most of the alt L1 ecosystems are struggling. Their struggle can be attributed to a lot of factors, but one thing that is clear is that there is significant room for improvement. So what are the possible changes that can be made to improve these L1s?

As a more general solution towards all L1s, the main one would be working with teams to focus on improving the user experience, more specifically from the wallet perspective. Once it becomes easier to self-custody assets and interact on-chain, there will automatically be a greater uptick in user activity.

Another suggestion would be to narrow the focus. Rather than trying to be a chain that facilitates everything, it would be good to understand your own unique benefits and the projects that work the best on your chain and foster an environment that allows those to shine the most. That will help the chain grow with a strong foundational use case.

Another point of focus, especially for the newer and trendier alt L1 chains is to focus on decentralization. The reliance on VC funds and a small number of validators for the success of an L1 ecosystem has proved to be problematic. To have long lasting success one must remove as many potential centralized points of failure as possible.

Apart from that, attention in the crypto market is generally low right now. To effectively chip away at Ethereums market share, an Alt L1 needs to be the chain where something new happens. DeFi, NFTs, and gaming all started on Ethereum and got copied elsewhere. A chain that creates something unique and allows that to flourish will put itself in a spot to capture existing crypto natives as well as some completely untapped markets. The only L1 that has done something like this so far is Arweave with decentralized storage. If any other Alt L1 can do this, they will put themselves in a strong position to compete with Ethereum over the coming years.

Concluding thoughts

Through 2021, a whole suite of L1 chains spawned and a number of them saw spikes in usage and adoption through the year. However, the year 2022 has been quite the opposite. As more than $2 Trillion of marketcap got wiped out of the crypto ecosystem, some of the alternative L1 chains have faced stress tests like never before. The result has been an exodus of users, capital, and liquidity that is returning to the safety of Ethereum.

This combined with the rise of layer 2 rollup chains puts into question whether the alt-L1s will be able to compete with Ethereum’s stickiness. If L2 rollups prove to be the answer for scalability, then Ethereum would have successfully solved the trilemma. This begs the question whether in the future we see a “Battle of the L2s” or do the Alt-L1 platforms find a way to innovate and continue to challenge Ethereum’s dominance?

Only time will tell.

Thank You for Reading.